Retire in 6 Years with 625k in savings

I’m 31 years old. I’ve had a bunch of different jobs. Teacher, actuary, travel guide, etc.

In my 20’s, I didn’t really know what I wanted. I found a great job out of college at a massive company but I only lasted 2 years because I hated the office life and wanted some more excitement out of life. “Retirement” was still a fuzzy concept that I could not conceptualize at this point.

I took a 50% pay cut to work as a Math teacher in an awful school, and I continued to make rash but exciting decisions like this one for the next 4-5 years.

If I would have known back then what I know now, I could have been retired by now. But I didn’t – and hindsight is 20/20.

Fast forward to now. (early 2025) I’ve found myself at a fully-remote corporate job making 108k per year. (a pretty good deal) While I don’t necessarily enjoy the job, something tells me I should ride this thing out until I can pull off an “extra lean FIRE”.

My least favorite thing to do in the world is work for a corporation. This is “soul-crushing” to me.

My favorite things in the world are free (being outside, sports, conversations, reading, etc) and I’m more than willing to live off very little money so that I can spend more time doing the things that I like doing, and less on things I HATE.

My goal is to save up a (small) pot of money so that I don’t have to do this anymore. It’s not that I don’t want to “work”, but rather I want to work on things that I want to work on.

Once I have money saved up, I’d be more than happy to work doing something enjoyable.

Retire in 6 years

How much do I NEED to live on per year??

In today’s dollars, let’s say $2,000 per month, or $24,000 per year. Just to make it easier, let’s say $25,000 per year.

So, if I can amass a portfolio of $25,000 x 25 = $625,000 I could theoretically live off the 4% interest annually. (4% of 625,000 is $25,000)

If I assume a more generous rate of 5% interest to live on annually, I could theoretically live on $25,000 x 20 = $500,000.

What Do I Have NOW?

I’m 31 years old. On April 22, 2025, after some pretty big market hits these last few weeks, here is what I have:

| Roth IRA | $98,000 |

| Rollover IRA | $24,292 |

| HSA | $15,172 |

| Total | $137,470 |

Update 5/20/25: Portfolio is at $165,074 now. I originally wrote this when the market was at an all-time low!

What Kind of Job Do I Have?

I just started a new job. My salary this year is $98,000 + $10,000 bonus for a total of $108,000. I may receive a bit more in bonuses this year and in the following years, and I’ll definitely see salary increases, so I’ll try to account for these things.

What’s My Take Home Pay?

Base of 98k + 10k bonus = 108k

Taxable Income = 108k – 4.3k hsa – 23.5k 401k – 14.6k standard deduction = $67,600

updates 5/20: adding another 7k to my ira will reduce taxable to 60,600.

- also, employer match of 6% after year 1 will mean I will only contribute 17.5k of my money to 401k and employer will contribute 6k. meaning another 6k will be freed up to invest – I didn’t take this into calculation earlier.

Federal Tax = $9,925

- will actually be lower than this

MA State Tax = $3,890 (flat 5% on $77,800 – MA doesn’t do standard deduction)

FICA = $8,415

Health Insurance = $1,638

SO… 67,600 – 9,925 – 3,890 – 8,415 – 1,638 = $43,732 take home pay

What are my recurring expenses?

Rent – $1550 per month x 12 = $18,600

Utilities – $100 per month x 12 = $1,200

Car Insurance – $274 per 6 months x 2 = $548 per year

Food – $200 per month (guess – need to calculate this exactly)

Gas – $50 per month (gas is cheap in Boston – I work from home – should I sell my car?)

Total Recurring Expenses – $20,598

What SHOULD I Have Left Over?

With a take home pay of $43,732 minus recurring expenses of $20,598 that gives me $23,134 left. With that, I should be able to invest about $18k in a brokerage account (or maybe 7k in a Roth as well?? still not sure yet), while keeping about $5k liquid for bills, emergencies, etc.

- update is that 7k will go in a traditional ira to reduce my taxable income by 7k. no Roth because focusing on reducing my taxable income – I can live off way less than 100k (my current salary) once I retire.

What’s my Plan?

In order of priority, here is my plan for this year.

1 – Max out HSA – $3,925 employee + $375 employer = $4,300 total

2 – Max out 401k – $23,500 (no employer match first year, after that match at 6%, so I’ll be contributing $22,169 and employer will give $1,331)

3 – Max out Roth – $7,000 (EDIT 5/6/25: I think I should max out traditional IRA actually. Reduce taxable income even more – this will change my growth as I won’t be losing any of this 7k to taxes)

4 – Put remaining money in brokerage account

So When the hell can I FIRE?

This calculation is tricky. I need $625,000 to produce an annual income of $25k. Let’s assume I can live on 25k per year.

I have $137,470 now all in a Roth and HSA. Meaning I’m $487,530 short by my calculations.

Where am I going to get $487,530 from for god sake??

My Next 5 Years

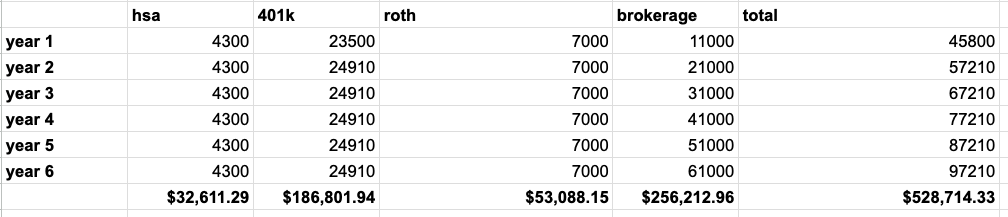

For fun, I put together a quick spreadsheet to see roughly what my savings would come to if I work 5 more years at this job. For the sake of this exercise, I assumed a 7% rate of return, which I got from 10% per year minus 3% per year for inflation. Maxing out HSA, 401k, and Roth every year, while increasing my brokerage by 10k each year due to wage increases by 10% each year. (my current gross is 108k per year) As you can see, at the end of 5 years I’ll have $397,170.38.

So, what happens if I bump it to 6 years? It looks like I’ll be at a crispy $528k. Since I decided above that I need $487,530 minimum to retire, I’ll be there in 6 years if I stay the course.

Can I Speed Up These 6 Years?

I made a lot of assumptions when doing these calculations, and it has occurred to me that I could definitely speed up the process. Here are some things I could change.

Decrease my housing costs

I currently live in Boston and pay a decent amount for housing. (see my post on Boston Cost of Living) I could move somewhere cheaper, dog sit, live with my parents, or live out of a van. All of these would lower my housing costs by a substantial amount. I will certainly be looking into these things in the upcoming months.

I work fully remote and can work anywhere in the continental US. I would love to work from a low-cost place abroad – but I’m not sure that’s possible with my current company, though I haven’t tried it! I currently don’t want to ask permission in case I am denied, because then I definitely won’t be able to try it. If I try and am caught then at least I can say I didn’t know.

If I can decrease housing, then I can put WAY more into a brokerage, and BUST up out this job WAY sooner!

Move to a State with No State Income Tax

Currently I live in Massachusetts which has a flat 5% state income tax. In my calculations, I have myself paying $3,890 this year to the state. If I moved to a state with no income tax, I could invest all $3,890 of that and let it grow for years!

I could move to Florida, Nevada, South Dakota, Texas, Washington, or Wyoming. I have to admit, this is very enticing.

$3,890 in 20 years from now at a 7% interest rate is $15,053! Plus, the taxes I owe Mass. is only going to go up as I make more money annually. Just living in Mass for one year will cost me $15,053 in future dollars 20 years from now.

Increase my income

There are many ways I could do this. I could coach a soccer team at night. This could add another 10k ish to my annual income. I’m debating whether this would be a good idea. I love soccer and working with kids (I used to be a Math teacher), but it is demanding on nights and weekend. Is the commitment worth the loss of time? Maybe.

I have a travel blog that makes a very small amount of income right now – so small that I didn’t even factor it in to these calculations. If this picks up, I could definitely retire sooner!

Realistically, these are my two options. I already have a 9-5 that pays decent, so its not like I have a TON of time to do other things. Either I coach a soccer team at night, or start making more money on my travel blog. Or, just maybe, this blog will make me some money one day!

Summary – Retire in 6 years

Does this make sense?

If I can accumulate 625k in savings, I’ll generate 25k in passive income annually, which would give me $2,083.33 per month to live off of in today’s dollars. Since these would be capital gains, I would maximize my tax strategy so that I pay no taxes on this money. (thanks go curry cracker!)

Is this a lot of money to live off of? No. Could I make it work so that I don’t have to be a corporate slave until I’m 60? Most definitely.

I’m 31 now, in 6 years I’ll be 37. Hopefully by then I’ll have a kid and will have tons of time to play with him or her! I definitely do not want to have to pay to send my kid to daycare while I go to work.

It’s important to remember, I’m not opposed to “working”. I just don’t want to be a corporate slave.

I’d be more than happy to work as a soccer coach once I “retire” to supplement my income. Or do some teaching. Or live abroad for a while in Central/South America/Asia/Europe. I’ve done a ton of traveling already and understand exactly what that would be like.

What did I miss?

Sam